Market Outlook November 2023

While the outlook for the economy as a whole is fairly pessimistic for the next couple of years, forecasters expect the construction sector to be relatively resilient.

Whilst output is expected to fall over the year ahead a gradual recovery is expected from 2025 onwards. Inflation (CPI) in September was 6.7% per annum, down a further 1.2% from June.

However even with further reductions forecast over the upcoming months, it is still well above the Government’s 2% target, a level it is not expected to return to until 2025 at the earliest.

This could lead to further interest rate rises by the Bank of England, possibly to 5.5% and then remaining at a higher level than previously forecast for longer.

Market Outlook

Looking at the UK as a whole, the market is changing as input cost pressures ease and demand softens, which should lead to more competitive tender returns allowing investors to take marginal projects forward to construction. This is now becoming more evident locally, with several instances of contractors enquiring about tender opportunities as a result of resource availability in 2024.

Although the UK Economy is likely to avoid technically going into recession this year, overall economic performance has been poor when compared with other G20 nations. The indicators for economic activity show that the economy is losing momentum with a contraction recently seen in the manufacturing Purchasing Managers Index for the first time this year.

The following forecasts are based on a middle of the road set of assumptions with regards to trade restrictions and subdued economic performance by the UK economy as a whole. However, the figures could vary by up to 15% (+/-) per annum over the period of the forecast depending on the medium-term implications of Brexit on trade, the extent of continuing material shortages, and any escalation of the war in Ukraine.

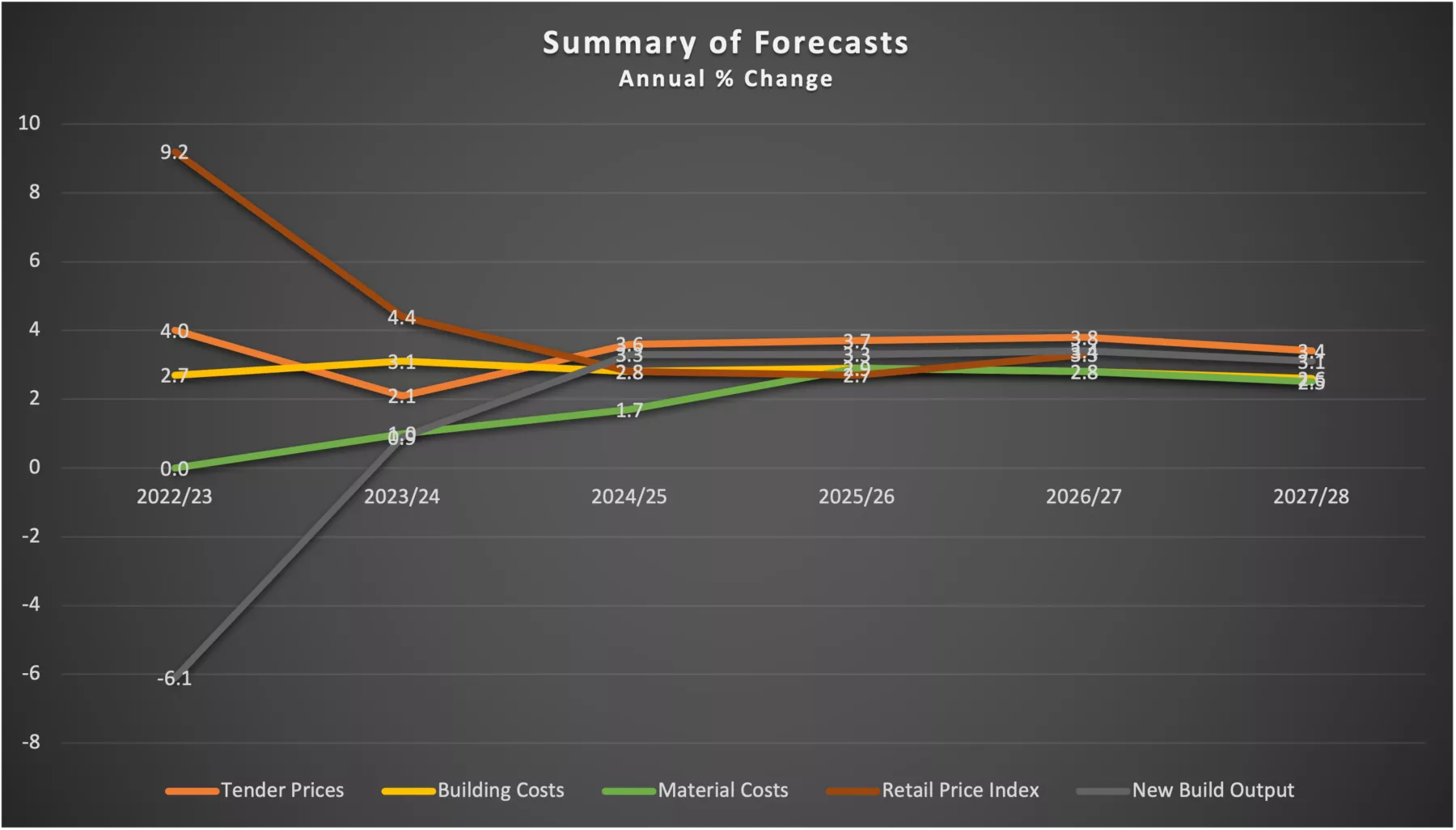

Summary of Forecast

The forecast movements in construction costs currently shown in the BCIS Quarterly Report are as follows:

Tender prices rose by 0.8% over the last quarter. However, the annual rise dropped by a further 0.9% to 4.0% when compared with the same quarter in 2022. Tender prices have been rising since the second quarter of 2020, but the rate of increase is now forecast to reduce further to 2.1% by autumn 2024 driven by easing cost pressures and less demand.

The forecast for the following 4 years indicates tender price increases of around 3.6% in 2025 and 3.7% per annum over the remainder of the forecast period. Decreasing demand and fewer opportunities will lead to more competitive pricing, with tender prices only rising faster than costs from 2026 onwards, as contractors absorb some of the predicted increases in costs in the short term. Over the next five years tender prices are currently forecast to rise by 18% overall, a 3% decrease compared to the last forecast.

Building costs rose by 0.5% in the last quarter when compared to the previous quarter and by 2.7% from the same quarter a year ago, a further significant reduction from the peak of over 14% seen in mid-2022.

Overall, costs are expected to continue to rise over the next 5 years, with increases around 2.7% in 2023 and then remaining at a similar level from 2024 for the remainder of the current forecast period. Building costs are forecast to rise by 15% in total over the next 5 years, a reduction of 1% from the previous forecast.

Total construction output increased by 4.4% in 2022. New construction work is expected to reduce by up to 6% over 2023-2024. Growth is expected to return in 2025, with an overall increase of 6% over the period to 2028, driven by increasing investment in the infrastructure sector.

Conclusion

The market appears to be shifting towards the buyer with demand falling in the public sector as budget cuts take effect. This should see a more competitive tendering environment as contractors actively seek opportunities to secure cashflow for the next couple of years.

Sign up for news

Receive email updates from Thomson Gray direct to your inbox:

- Subscribe to Practice News

- Subscribe to Market Outlook