Market Outlook October 2025

The outlook for the UK economy remains challenging for the rest of this year and most of 2026, but with better overall growth in GDP now forecast from 2027 onwards.

The latest GDP forecast is an increase of 1.3% for 2025, and 1.1% for 2026, before average increases of 1.75% from 2026 to 2029. Inflation forecasts are currently 3.6% at the end of 2025, before reducing gradually and reaching the Bank of England’s 2% target in mid-2027.

Recent data from the S&P Global UK Construction Purchasing Managers Index (PMI) indicates a marginal increase in overall construction activity. After falling below the neutral 50 mark in January and February, the index has risen for five consecutive months, though it remains below 50 – the threshold between growth and contraction.

This modest improvement reflects an uptick in new work orders and output, suggesting a tentative recovery in sector sentiment.

While the UK Government’s recent spending review was broadly positive for the construction industry, promising increased investment in built assets over the next decade, no significant new projects or opportunities have yet materialised.

Simplification of planning and other regulations was also noted, but meaningful progress remains limited, with little evidence of measures to stimulate private sector involvement either directly or through public-private partnerships.

The Bank of England’s recent 0.25% reduction in the Base Rate, bringing it to 4%, appeared somewhat counterintuitive, given the simultaneous increase in CPI inflation to 3.8%, largely driven by higher food prices.

Further reductions in Base Rate now appear unlikely, and despite a stated desire to stimulate growth, both domestic and global economic uncertainties persist.

It is therefore likely that in the short to medium term, the bank will adopt a more cautious approach as inflation is now expected to remain above the often stated 2% target until late 2027.

Local Outlook

Looking at Scotland in general, the construction sector continues to suffer from a lack of clarity on future opportunities. The view on anticipated pipelines of projects going to tender over the next 12 months is improving from the last two quarters, with 40% of companies forecasting an increase in opportunities, a further 40% an unchanged position and the remaining 20% predicting a reduction.

Contractors’ interest in tendering for projects remains mixed. Although fewer contractors are actively seeking new tenders than in previous forecasts, most consultants are still able to assemble an appropriate tender list.

Larger contractors continue to show a preference for two-stage procurement, reflecting a desire for greater cost certainty and improved risk management. In contrast, the subcontract market remains more short-term in focus, influenced by capacity constraints and concerns about holding prices over extended pre-construction periods.

The BCIS Scottish Contractors Panel reports that overall demand levels continue to decline, with fewer opportunities emerging across both public and private sectors. Delays to the Scottish Government’s National Planning Framework 4 have had a significant impact, resulting in limited visibility of the future project pipeline. This situation is very similar to issues faced in the rest of the UK around five years ago.

Tender interest continues to vary significantly by location, with greater competition evident in the central belt compared to the North East and South of the country. Main Contractors are also experiencing different levels of premiums in the Highlands & Islands, although this can vary considerably between various trades and project locations.

Both Scottish BCIS panels have highlighted the need for more skills training and apprenticeships to strengthen the future talent pool and avoid impending labour resource issues. Additionally, statutory approvals, funding constraints and utility procurements were also noted as significant ongoing issues, affecting both programming and cost of potentially viable projects.

Summary of Forecast

The following forecasts are based on a mid-range set of assumptions regarding trade restrictions and economic performance by the UK economy. However, the figures could vary by up to 15% (+/-) per annum over the period of the forecast.

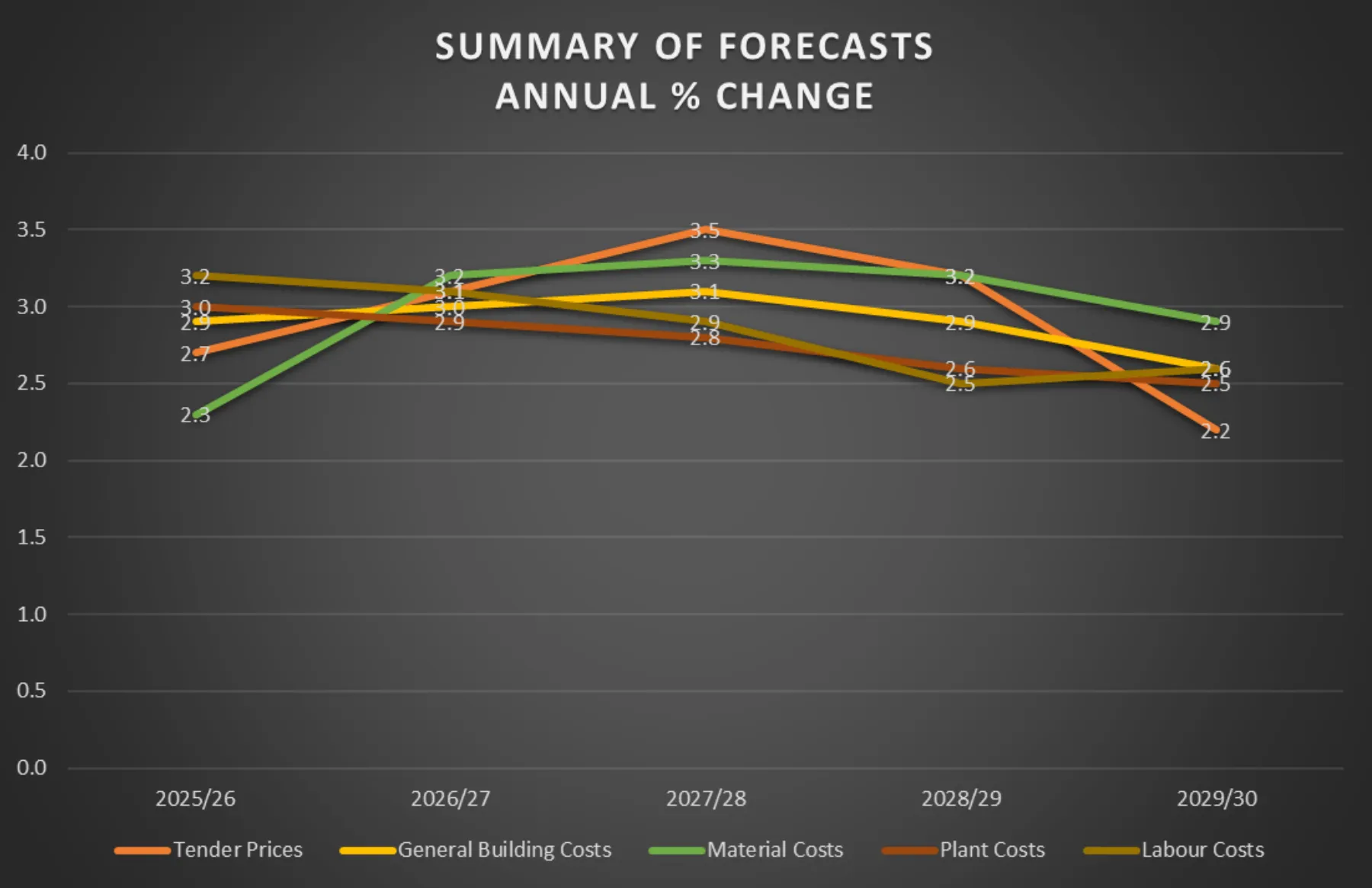

The forecast movements in construction costs currently shown in the BCIS Quarterly Report are as follows:

Overall, UK Tender prices increased by 0.7% over the last quarter, with a similar 0.7% rise recorded in Scotland. On an annual basis, tender prices rose by 2.5%, up 0.2%. In Scotland, the annual increase was 2.9%, down from 3.4% when compared with the same quarter in 2024.

The overall sentiment of the UK Tender Price Index (TPI) panel has continued to improve since the last quarter, reflecting expectations of a growing pipeline of work over the next year. Tender prices are currently forecast to increase gradually, peaking at around 3.5% in 2028 before easing slightly towards the end of the forecast period.

As in the previous two quarters, a clear differential remains between tender price movements for M&E and general building works. Labour costs continue to be the main factor for increases, with material cost increases becoming more stable as supply issues decline.

In Scotland, this remains widespread given ongoing labour shortages and regional disparities between the central belt and more remote regions. This has led to continued variability in tender pricing depending on project location and resource availability.

Competitive pricing levels continues to decline slightly from the previous quarter, as contractors become more selective on what they will price. Over the next five years, tender prices are forecast to rise by approximately 14.7% overall, a 0.3% increase compared to the last forecast. This rate of growth remains broadly in line with expected building cost inflation, although concerns persist regarding the future project pipeline and the sustainability of demand across certain regions and sectors.

Building costs rose by 1.7% over the last quarter compared with the previous quarter, including a rise of 1.0% identified in Scotland, and by 3.5% from the same quarter a year ago (3.1% in Scotland), giving similar annual increases as reported in the last forecast.

Looking ahead, building costs are forecast to rise by approximately 14.5% in total over the next five years, a 0.5% decrease compared with the previous forecast, with more moderate increases in labour and material costs still being anticipated.

In Scotland, costs for direct labour, materials, and subcontractors all decreased over the last quarter, while plant costs increased by 2.3% since Q2 2025.

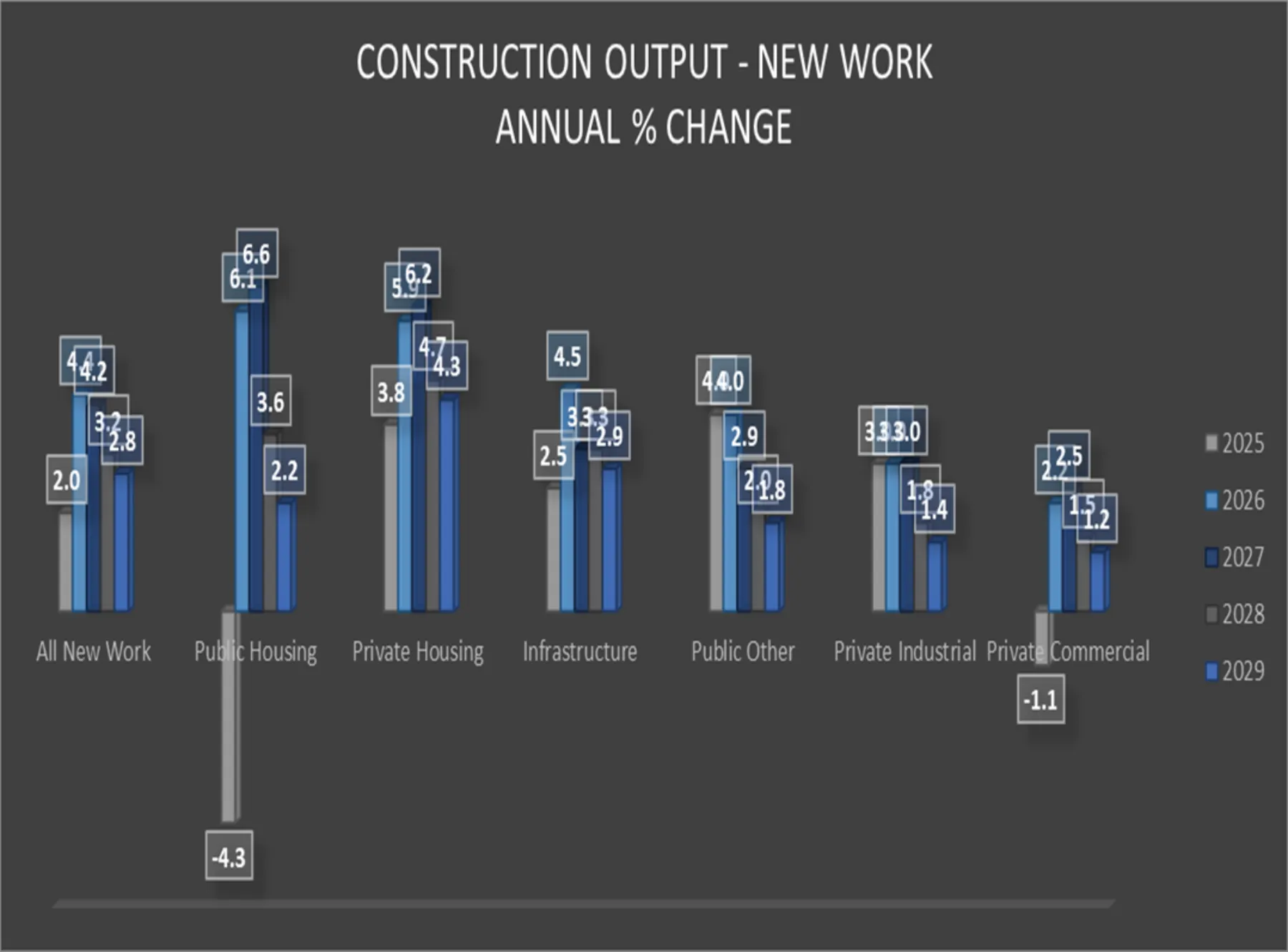

Construction Output

New work output declined by 5.1% in 2024, with growth of 2.0% forecast for 2025, followed by higher increases of 4% per annum over the next couple of years, driven predominantly by the housing and infrastructure sectors, but with private industrial and commercial forecasts remaining subdued.

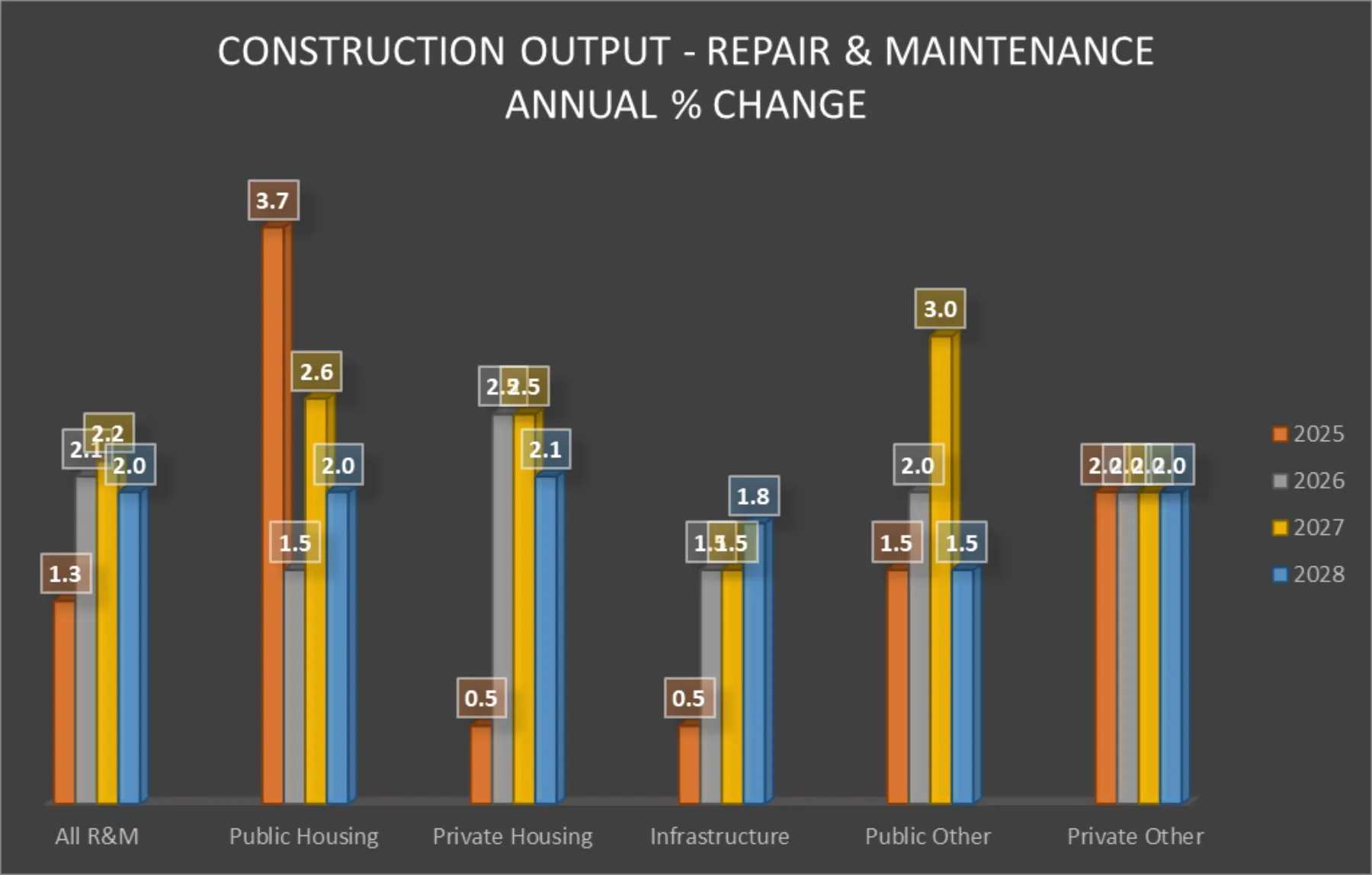

There was, however, a less positive picture for the Repair and Maintenance sector, with only a modest annual increase of 1.5% forecast for 2025, following a positive 8.7% growth in 2024.

Growth rates are expected to grow slightly over the period of the current forecast, driven mainly by the public sector. Annual increases are expected to range from 1.5% - 2.6% as shown in the graph below.

Conclusion

The market views in construction have improved further since the last forecast, with only very limited (sector-specific) output growth evident in 2025 before sector-wide growth returns in 2026 and accelerates from 2027 onwards.

Whilst there is some cause for optimism, current signs of declining orders and any delay to major project pipelines could challenge the financial stability of companies across the industry through the combination of smaller workloads, rising costs and the associated reduced margins.

Overall, it remains a challenging period for the Construction Industry.

Sign up for news

Receive email updates from Thomson Gray direct to your inbox:

- Subscribe to Practice News

- Subscribe to Market Outlook