Market Outlook February 2026

The UK economic outlook for 2026 remains challenging, although growth prospects from 2027 onward have improved. GDP increased by 0.1% in the final quarter of 2025 and by 1.3% over the year.

Forecasts projects growth of approximately 1.2% in 2026 (OECD) and 1.1% (IMF), followed by average annual growth of around 1.4% from 2026 to 2029, down from 1.75% in the previous round of forecasts.

There has also been significant shift recently in the amount of construction activity over the UK wide sector. The December update to the S&P Global UK Construction Purchasing Managers Index Survey suggested that the construction sector is experiencing its largest downturn in more than five years. Despite this, long-term positive sentiment was clear, albeit at a slower rate than was both anticipated or hoped for.

The Construction Products Association (CPA) has also revised its 2026 Construction Output Forecast downward from 2.8% in October 2025 to 1.7% in January 2026.

The reduction in growth is attributed to rising risk aversion across the industry. The CPA noted there are a variety of factors that contribute to the stagnation of growth with geopolitical developments being identified as a key example.

The Bank of England’s December decrease in Base Rate by 0.25% to 3.75% reflects a view that inflationary pressures are now ‘less pressing’ with the aim of holding fire until the longevity of reductions in the headline rate of inflation becomes clearer in. Further cuts in Base Rate are now expected during 2026, with the rate forecast to fall to around 3.25% by year-end, alongside an inflation projection of 2.2%, still above the stated target of 2%, but 1.2% lower than previous forecasts.

Local Outlook

In Scotland, the construction sector continues to face limited clarity on future opportunities. The view on anticipated pipelines of projects going to tender over the next 12 months has fallen from 40% to 32%, while 50% now expect no change (up from 20%). The remaining 18% predict a reduction falling by 2%.

Logistical challenges remain with the Scottish Consultant’s Panel highlighting labour shortages, sub-contract pricing and finance/funding issues still impacting on private and public sector developments. The BCIS Scottish Contractors Panel report slight improvements in demand but considered it unlikely that numerous projects would be imminent.

Frameworks and negotiation were noted to be the preferred procurement route, with little appetite for single stage competitive tendering. Also noted were short tender periods on design-and-build projects, leading to lack of interest and increased costs to cover design risk.

Tender interest appears to have improved over the last quarter with more consultants able to source their required number of tenderers. However, the increasing number of opportunities is giving specialist sub-contractors more ability to select which project to pursue, in some cases leading to increased costs.

Both Scottish BCIS panels noted that persistent labour shortages continue to pose challenges, with a shortage of college places for skills training and apprenticeships becoming a longer-term issue for the industry. Overall, the current position and short-term outlook remain broadly unchanged, with only marginal improvements since the previous quarter.

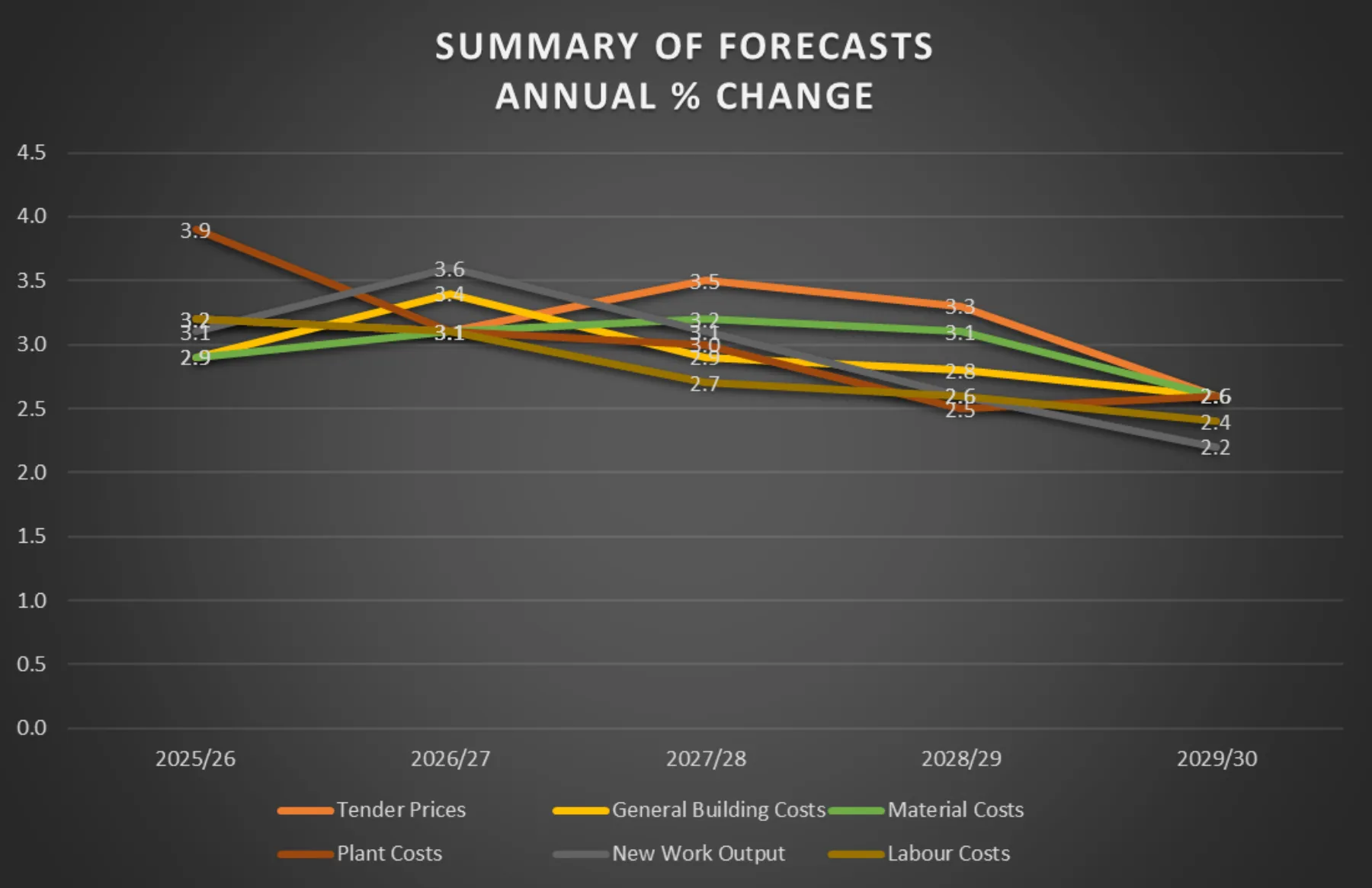

Summary of Forecast

The following forecasts are based on a middle of the road set of assumptions with regards to trade restrictions and economic performance by the UK economy as a whole. However, the figures could vary by up to 15% (+/-) per annum over the period of the forecast.

The forecast movements in construction costs and output currently shown in the BCIS Quarterly Report are as follows:

Tender Prices

UK Tender prices rose by 0.7% over the last quarter, with a rise of 1.0% in Scotland. Annual growth remained at 2.5% for the UK and 3.1% in Scotland, up from 2.7% in the previous forecast, when compared with the same quarter in 2024.

The overall view of the UK TPI panel continues to improve from the sentiment reported last summer. Approximately half the panel believed there was an increased pipeline of work expected over the next year, but this is not yet being reflected in output figures as more projects were put on hold ahead of the Autumn Budget.

Tender price increases are forecast to rise to 3.5% in 2028 before dropping below 3% towards the end of the forecast period. Over the next five years, tender prices are currently forecast to rise by 17% overall, a 2.3% increase compared to the last forecast.

Labour Costs

Labour costs remain the key driver for cost increases, with rises above the rate of inflation. Skill shortages are still evident, particularly in white collar professions, but with a recent reduction in job opportunities being seen by the Office for National Statistics. BCIS forecast that labour costs will rise by approximately 15% over the next 5 years.

Material Costs

Material cost inflation has stabilised over the last couple of years following the easing of previous logistical pressures. BCIS predict an overall rise of 16% over the current forecast, with significantly increased activity being the main risk to the forecast.

Plant costs

Plant costs are also expected to increase by around 16% over the next five years, a slower annual growth rate than earlier forecasts.

Overall Building Costs

Building costs rose by 4.5% from the same quarter a year ago (4.5% in Scotland), giving higher annual increases as reported in the last forecast. Building costs are forecast to rise by approximately 15% in total over the next 5 years, an increase of 0.5% from the previous forecast, with labour supply still a major concern.

Construction Output

New work output increased by 1.8% in 2025, though sector performance varied widely from +19% in private industrial and public non-housing) to -9% in private commercial. Growth of 2.0% is forecast for 2026, with stronger growth of 3-4% annually in subsequent years, driven predominantly by the housing and infrastructure sectors, but with private commercial and public housing forecasts staying subdued.

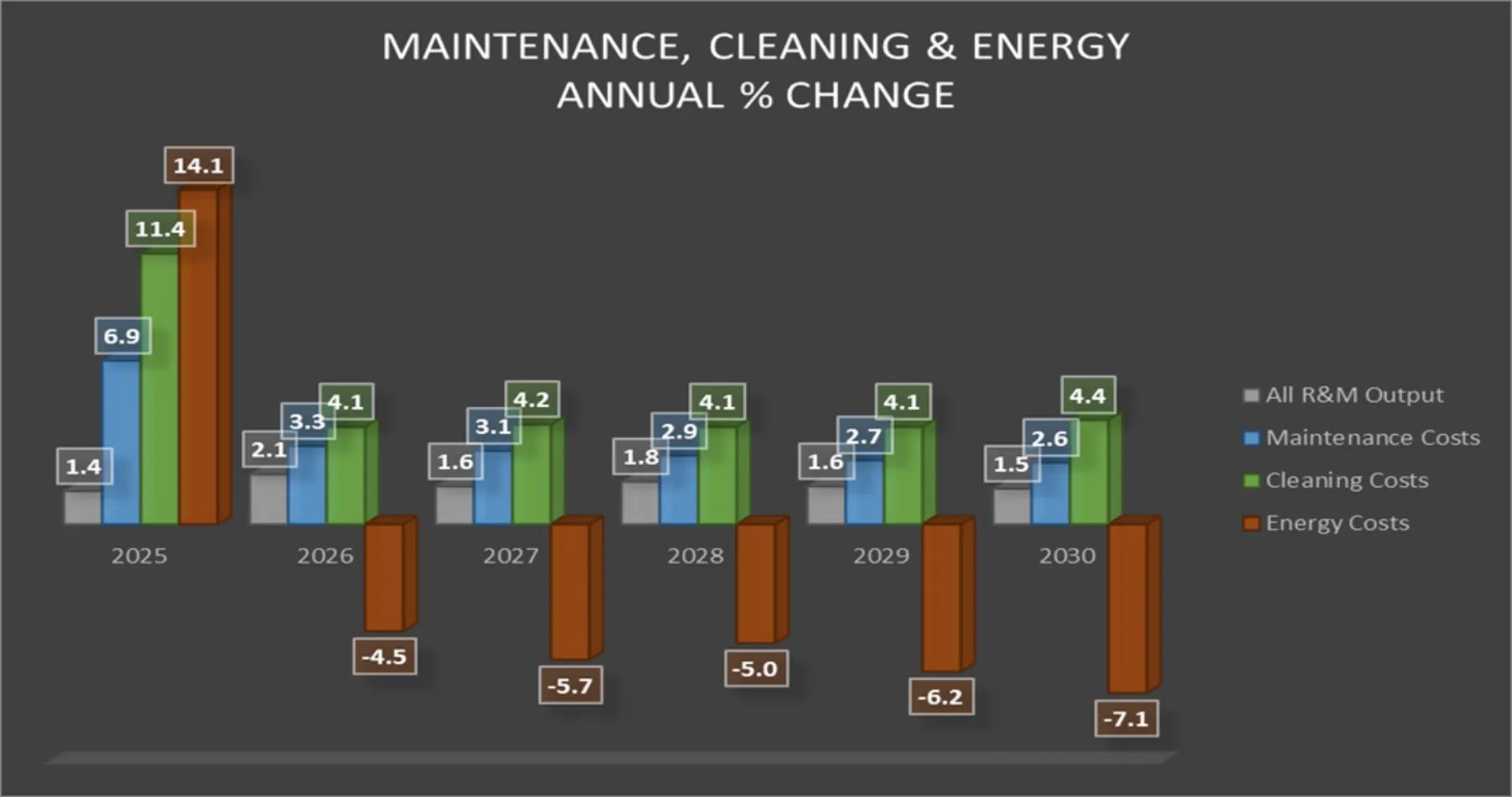

Repair & Maintenance, Cleaning and Energy

Facilities maintenance activity continues to be constrained by increasing labour costs and funding issues, with more emphasis being placed on improving efficiency and reducing expenditure.

Output and costs are both forecast to rise but at more moderate rates than seen over the last few years. The exception to this is energy costs which are forecast to fall significantly over the next 5 years after an increase of over 14% in 2025.

Forecasts for the next 5 years are shown in the graph below:

Conclusion

The UK construction sector enters 2026 in a delicate position. The key variable is still timing. The sector's interest-rate sensitivity means it should be among the first to benefit from cheaper borrowing, potentially reviving stalled projects and improving development viability.

Activity has recently softened; confidence is still muted and challenges around planning and skills persist. Yet the general economic environment is moving in a more favourable direction than seemed possible towards the end of 2025.

The impact of the December rate cut, followed by expected further easing through 2026, provides a tangible basis for optimism for an industry where project viability is closely linked to financing costs, but the pace of that recovery will be incremental and both sector specific and geographically uneven.

Sign up for news

Receive email updates from Thomson Gray direct to your inbox:

- Subscribe to Practice News

- Subscribe to Market Outlook